What happened to labor market dynamism?

February 24, 2026

In economics, markets are defined by their price and quantity.

Over the last two weeks, I’ve been talking about the labor market, specifically its quantity of jobs and the price of those jobs as defined by pay.

Looking at these elements together, two things become clear.

Over the last three years, hiring has slowed sharply. And while pay growth has stabilized at levels higher than those seen before the pandemic, the payoff from changing jobs has fallen to its lowest level in ADP data going back to 2017.

What this means for the labor market is that workers and employers, for now, are sticking together. To quantify this job stickiness, we measure the number of quits and layoffs divided by the total level of employment in the previous month to get the rate of employee turnover.

Since the Great Resignation of 2021-2022, the pace of turnover has slowed steadily. In January, it was at its lowest level in nine years.

Nowhere is this employment standstill more apparent than in white-collar jobs. Take the examples of finance, information, and professional business services, where most jobs are held by knowledge workers.

These sectors have made headlines recently as advances in artificial intelligence both augment employment (through demand for developers, for example) and curtail it (by automating tasks).

Turnover in these sectors was modest in January compared to a year ago.

In finance, worker separations held steady. In information and professional business services, turnover slowed from a year earlier. In professional business services, the pace of turnover in January was the slowest we’ve recorded for that sector for the month.

My take

The pandemic was declared over in 2023, but the labor market continues to be shaped by its dramatic employment losses and their rapid recovery, when employers couldn’t hire workers fast enough after widespread quits and layoffs.

That experience has yielded to a more cautious approach to both hiring and firings, with employers doing less of both. For workers, the hyper-competitive labor market of the Great Resignation, which generated larger salaries and improved benefits, has been replaced by a stable, but softer employment environment.

The normal push-and-pull of job gains and pay growth—quantity and price—that once kept the labor market dynamic has weakened, giving way to a market defined more by inactivity than vigor.

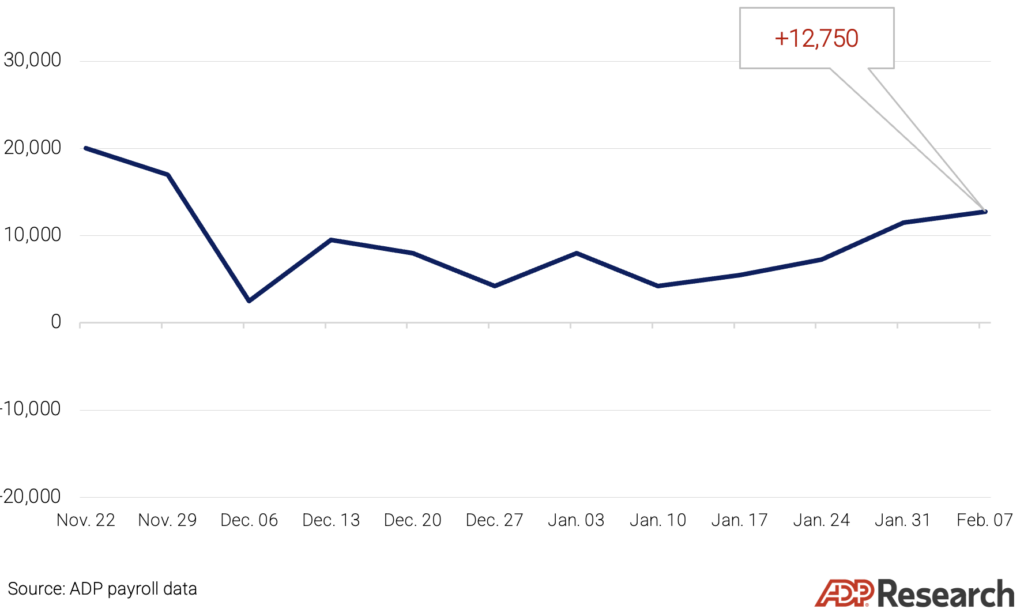

THE NER Pulse

For the four weeks ending February 7, 2026, private employers added an average of 12,750 jobs a week. It was the fourth straight week of strengthening job gains.

These numbers are preliminary and could change as new data is added.

About The NER Pulse

Three times a month, Main Street Macro releases the NER Pulse, an estimate of the week-over-week change in employment based on a four-week moving average. These releases are seasonally adjusted and have a two-week lag to allow for more complete and accurate estimates of real-time employment trends. At the beginning of each month, we publish the National Employment Report, which is built on a reference week that includes the 12th day of the month. We do not publish the NER Pulse during NER release weeks.

Download this week’s NER Pulse data

The week ahead

Tuesday. This morning, we’ll get a check on the housing market from the S&P Cotality Case-Shiller U.S. National Home Price Index for December. Also, data from the Conference Board’s Consumer Confidence Index will show whether consumer confidence recovered in February after falling to its lowest level in a decade the previous month.

Thursday. Weekly jobless claims data from the Department of Labor likely will show that employers are keeping workers, with this signal of layoffs continuing to hover at historic lows. The datapoint to watch will be continuing claims, a high-frequency indicator of the ease or difficulty unemployed workers are having in finding new jobs.

Friday The headline of the week will be the delayed January read on the Producer Price Index from the Bureau of Labor Statistics. Increases in wholesale prices can bleed into the prices consumers pay, and their rise or fall could be an early sign of the direction of inflation in 2026.