MainStreet Macro: Is the glass half full or half empty?

April 12, 2021

|

8 min

8 min

by Nela Richardson, Ph.D

We’ve seen a lot of good news on the economic front, from local jobs to global growth. Yet many Main Streeters are still living with the pandemic’s destruction to their businesses, jobs and health. This begs the question: Is the economic recovery a glass half full or half empty?

Let’s start with global growth

Half Full: The world economy is expected to grow by 6% this year, according to a new forecast by the International Monetary Fund. That’s the fastest global growth rate in 40 years. It’s also a step up from the 5.5% expansion the IMF issued in January and the 5.2% prediction it released late last year as COVID-19 cases were surging in many parts of the world.

What’s behind the improved outlook? Good news, of course. Trillions of dollars in government aid, especially in the U.S., accelerated growth here at home and abroad. And it gets better, for us at least: The U.S. is the only country where economic growth is forecast to be even better than it would have been before the pandemic hit.

Half Empty: Growth, as we know, varies from country to country. As you’d expect, the IMF forecasts that poorer nations with more limited access to vaccines will be slower to recover–as a group, they probably won’t return to pre-pandemic output until 2023.

This is a sea change. Before the pandemic, those emerging markets led global growth, a trend that had the promise to reduce the wealth gap between rich and poor nations.

Even wealthy countries likely won’t be unscathed by the virus. Many won’t return to pre-pandemic levels until 2022, according to the IMF. When all is said and done, the global economy in 2024 is estimated to be 3% smaller than projected before the pandemic.

Next, the jobs market

Half Full: Last month, the economy shook off its winter slump and surprised economists with a blockbuster jobs report. Job gains were broad-based across industries. The unemployment rate edged down and the number of people lured back into the market edged back up.

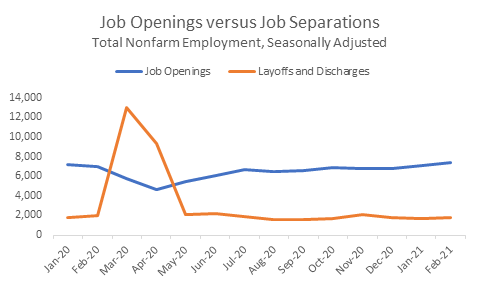

The Bureau of Labor Statistics gave us even more good news last week. Job openings in February increased by 268,000 to a total of 7.4 million – roughly the number of openings prior to the pandemic. Openings are a bellwether for future gains and give us a nice half-full perspective on the job recovery.

Half Empty: Yet the bounce in openings during the first two months of the year is far outweighed by the number of people who lost their jobs. Over the past year, hires totaled 72.3 million while separations were 80.9 million, implying a net employment loss of 8.6 million as of February.

And of those 8 million-plus people out of work, a huge percentage are long-term unemployed. More than 40% of them have been out of work for 27 months, a tenfold increase from before the pandemic, when the long-term unemployed made up only 4% of people out of work, according to the March jobs report. This stat is particularly alarming because the longer you stay out of the labor market, the harder it is to get back in. When and if you do, your paycheck probably will be smaller than it was.

Source: St. Louis Federal Reserve Economic Research

Last but not least, the service sector

Half Full: The pandemic has been particularly hard on service providers in industries that require close physical contact–think restaurants, shops and hotels. But the sector is poised for a big rebound in the coming months, according to the Institute of Supply Management survey of service sector executives, a closely watched measure of the industry.

The survey has signaled 10 straight months of growth in the outlook for services, with the March index leaping to a record high 63.7 from 55.3 in February. Index levels greater than 50 signal growth in coming months in areas such as new orders and employment.

Half Empty: Inflation has been incredibly subdued. But buried beneath the ISM’s sunny topline data was a warning that we’ve seen in similar manufacturing surveys: Prices are going up. Executives are reporting supply and labor shortages (labor!).

Core consumer prices have fallen in the past two months from already modest levels, but three things could trigger rising inflation: Supply shortages, unleashed consumer demand, and high federal debt. All are present, and the federal debt has the potential to grow. In the coming months, that could boost inflation and interest rates above the modest levels now enjoyed by Main Street businesses and their customers.

My take

So when it comes to the economic recovery, is the glass half empty or half full? The answer is both.

But economic optimists and pessimists both need to pay attention to what’s in the glass, because that’s what matters most for the recovery. Right now, the glass holds a complex cocktail of growth prospects and stubborn challenges.

The drivers of growth include unspent consumer savings that could springboard into future spending once the economy fully reopens.

Momentum in the vaccine rollout and the largesse of government and monetary stimulus, too, surely will boost the likelihood of a good economic outcome.

But this rosy outlook is clouded by the sobering reality of a stormy jobs market. The plight of the long-term unemployed will only worsen the longer they’re sidelined, and the jobs market can’t recover fully without them.