Nela Richardson, Ph.D.

It’s National Basketball Association championship season – longtime readers know I’m a fan – so this week I’m handicapping three head-to-head pay-data matchups to suss out the direction of the labor market.

Just as a scoreboard tells you something about the quality and grit of the teams on the court, pay growth reflects the balance, or imbalance, between labor supply and labor demand. Changes in pay can tell us something about the health of the labor market.

Let’s look at three pay matchups to see what’s up, what’s down, and what their performance can tell us.

Matchup 1: Base versus gross

For our first challenge, let’s pit the trajectory of base pay against growth pay. Base pay is a worker’s fixed hourly rate. Gross pay is the base rate plus variable bonuses, commissions, and other extra compensation

Employers don’t like to cut wages, so instead of raising them they frequently use one-time bonuses to retain employees when the labor market is relatively balanced, saving more permanent hourly rate increases for when the competition for talent heats up.

From 2022 to mid-2024, the labor market was extremely competitive, meaning there were far more job openings than people looking for work. As a result, base pay growth for job-stayers – that vast group of workers who have stayed with their current employer instead of jumping ship – accelerated more rapidly than gross pay.

As the labor market stabilized, base pay growth slowed and stabilized. Gross pay growth remained choppy until fall 2025, when it began to accelerate at a relatively steady pace, save for a slowdown in February 2026. That month, large and medium employers, which tend to pay bigger bonuses than small ones, contributed just 3,000 of the month’s 63,000 job gains, which might have accounted for the dip.

In May, base pay was up 3.1 percent year-over-year, and gross pay up 3.9 percent, ADP Pay Insights data shows. Though overall compensation is strengthening, the anchor of base pay has held steady.

Handicap: Tie game. The base-versus-gross pay matchup is consistent with a balanced labor market.

Matchup 2: Stayers versus switchers

In a competitive labor market, workers have more opportunity to boost their compensation by switching jobs. Since 2020, during periods of strong labor demand the pace of pay growth for this group – we call them job-changers – has soared. The gap between job-changers and job-stayers hit a high in April 2022 at 8.2 percentage-points.

Starting in August 2025, that gap had settled into a much smaller range of about 2 percentage points. It has stayed there since.

Handicap: Another tie. The evenly matched stayers and switchers squads are another signal of labor-market balance.

Matchup 3: Goods versus services

The behavior of different sectors can tell us something about the labor market.

Among goods-producing employers, May pay growth for job-changers has accelerated in the past 12 months, while service-sector pay growth for job-changers has been flat or even decelerating.

That means goods producers are showing more signs of labor-market strength than service providers, which is opposite of what we saw between 2022 and 2024, a period in which services, led by leisure and hospitality, dominated pay growth.

Handicap: In this showdown, the edge goes to Team Goods, which is showing early signs of a strengthening labor market.

My take

I love a competitive game, but so far this hiring season I’m not counting on any nail-biters.

The head-to-head data on pay growth is pointing to a tie between labor supply and labor demand instead of a clear winner.

In basketball, all games eventually end. In the economy, there is no final buzzer. In the never-ending sport of economic change, the current period has been a healthy matchup that suggests labor market stability for now.

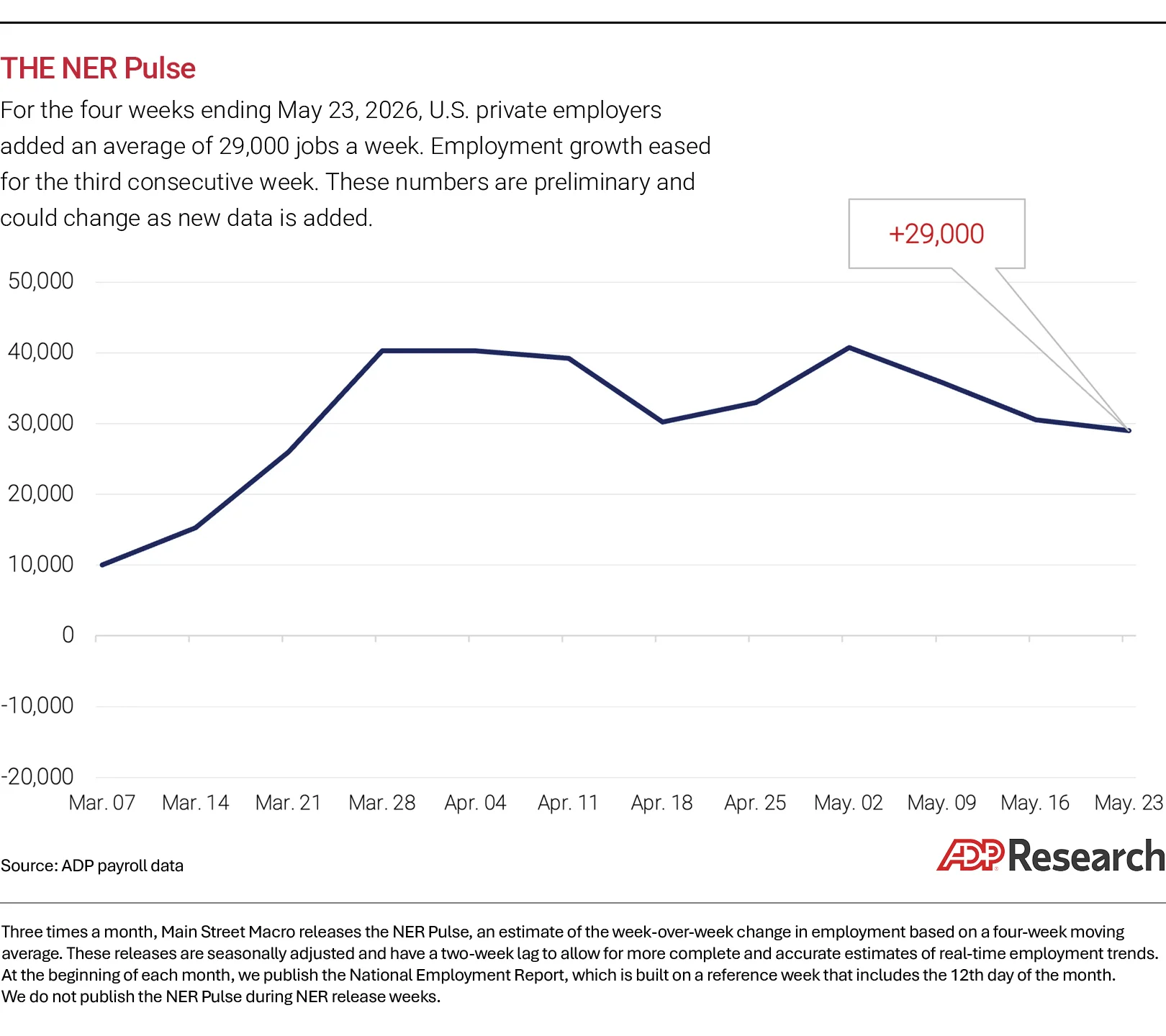

Download this week's NER Pulse data

The week ahead

Tuesday. So far, lower mortgage rates and accelerated wage growth haven’t been enough to overcome low housing inventory. Existing home sales in the first four months of 2026 are below what they were last year at this time. I’ll be looking for signs of a late spring thaw in the housing market when the National Association of Realtors releases May data on existing sales.

Wednesday. With the labor market on solid footing, attention will shift to inflation this week. In April, the pace of consumer inflation rose to its highest level in three years. Today, May Consumer Price Index data from the Bureau of Labor Statistics will tell us whether that surge was a passing spring shower or the start of a downpour.

Thursday. If inflation is indeed accelerating, we’re likely to see it first in prices paid by producers. The BLS Producer Price Index for May will be a gut check on Wednesday’s consumer data.

Friday. The week ends with an early read on consumer confidence for June from the University of Michigan. Its Index of Consumer Sentiment has been stuck on gloomy for more than five years now.